Forty years on: understanding the Appointed Representative Regime’s role in driving the next chapter of the UK’s Financial Sector growth.

A framework born of practicality

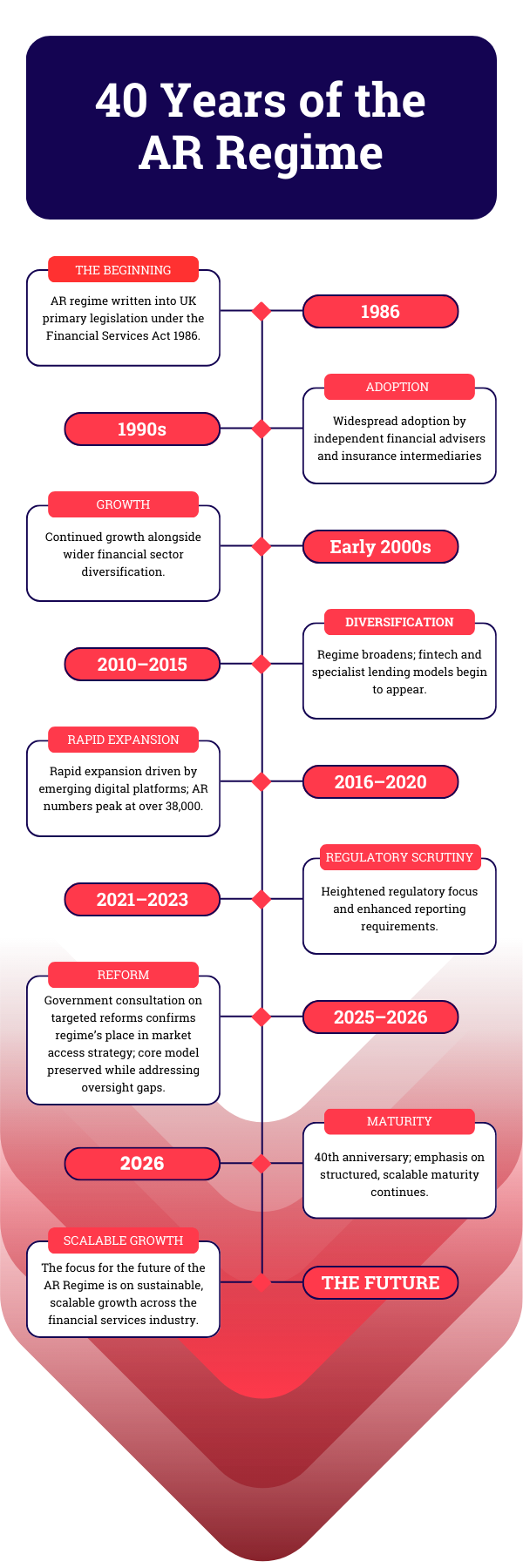

In 1986, when the Appointed Representative regime was written into primary legislation, it was introduced as a practical solution to a practical challenge. The UK’s financial services sector was expanding; independent advisers and specialists were emerging; and there was a clear need for a structure that allowed entrepreneurial, independent financial activity to flourish within a supervised environment.

What followed was not merely a regulatory mechanism. It became a catalyst for participation, and, eventually, for innovation.

Fast forward to 2026, and the regime remains deeply embedded in the fabric of the British financial services industry. At a moment when the country is actively seeking to reinforce its position as a global financial centre, championing fintech innovation, digital consumer finance, and AI-enabled advisory tools, the AR model continues to provide something the market consistently demands: a credible, compliant and efficient route to market.

The regime’s longevity is no accident. It has endured not only because it is convenient, but because it manages a fundamental tension: supporting market access without compromising consumer protection.

Over four decades, that balance between agility and accountability has proven remarkably adaptable.

From supporting independents to enabling a thriving innovation ecosystem

The growth in both scale and diversity of the regime speaks for itself.

The growth in both scale and diversity of the regime speaks for itself.

According to the latest FCA data (September 2025), there are approximately 2,469 principal firms overseeing around 34,012 appointed representatives in the UK today. This reflects a sizeable community of firms operating under principal oversight, spanning sectors that are far broader than the model’s original advisers and insurance broker roots.

ARs contribute significantly to economic activity. Recent data shows that, in 2024, the total regulated revenue associated with AR activity was £11.1bn, with an additional £27bn in non-regulated activity.

This scale has meant the regime has evolved well beyond its early role. The regime allows Fintech start-ups to experiment with new products, consumer finance platforms to build market traction quickly, specialist lenders and asset managers deploy new strategies, and international firms to use principal-host models to enter the UK market swiftly.

Some of today’s most recognisable financial brands began life under the oversight of a principal firm.

The regime has genuinely enabled market participation for independents and startups, and driven innovative industry growth.

A national growth agenda meets regulatory maturity

As the regime enters its 40th year, it does so against a backdrop of explicit government strategy that places financial services at the heart of the UK’s economic growth ambitions.

The government published the Appointed Representatives Regime consultation on 12 February 2026, building on the August 2025 policy statement that set out an overarching approach to preserve the regime while strengthening consumer and market confidence. The consultation is designed to refine how the regime operates, not to abolish it.

The government has made clear that:

- The AR regime “plays an important part in the provision of financial services” and delivers benefits to both businesses and consumers by expanding access to regulated markets.

- Proposed reforms will preserve the current broad scope of activities ARs can engage in, while enhancing consumer protection and oversight.

- Targeted changes include the introduction of a “regulatory gateway” requiring authorised firms to obtain specific FCA permission before acting as Principals, and reforms that enable the Financial Ombudsman Service (FOS) to consider complaints involving ARs where the principal is not responsible.

Importantly, those proposals make clear that the government does not intend to disrupt the existing core regime. Firms already acting as principals will be “grandfathered” into the new permission framework, ensuring continuity and stability.

This direction shows a pragmatic approach to reform: acknowledging legitimate concerns, responding to them, and preserving the operational benefits that make the regime vital.

Harnessing opportunity while addressing challenges

In recent years, the regulator has raised concerns about instances where certain principals’ oversight of ARs has not been as robust as expected, and this has unfortunately meant consumer and market harm has happened at a higher rate to their directly authorised counterparts. That has led to heightened regulatory attention, enhanced reporting requirements and deeper supervisory engagement.

Those developments might have felt unsettling to some over the last few years, but they reflect a broader truth about enduring frameworks: mature systems attract scrutiny precisely because they are important.

A model that underpins significant volumes of economic activity must be held to high standards, not to constrain it, but to preserve trust, confidence and long-term sustainability.

The government’s consultation explicitly frames the proposed reforms as targeted and proportionate, aiming to protect consumers and markets, while preserving the regime’s broad scope and economic benefits.

The evolving role of the Principal

Over four decades, the practical demands placed upon principals have shifted dramatically.

Where earlier AR oversight might have been lighter touch, involving site visits, reviewing physical files or quarterly reports, today’s supervision happens in an environment defined by digital communications, AI-enabled tools, remote client onboarding, and multi-channel engagement.

The composition of AR networks has also changed. Where advisory and insurance distribution once dominated, today’s AR cohorts include high-growth fintechs, tech-enabled lenders, digital wealth platforms, launching funds and strategies, and increasingly complex operating models.

That evolution has expanded both opportunity and responsibility. Principals today are more than permissions holders. They are enablers of innovation, guardians of consumer outcomes, and the custodians of market trust. Reputation is everything, and those principals coming out on top are the ones putting strong governance across their network at the core of their business.

The regime has always required that oversight be equivalent to supervising in-house activity, and that remains true in 2026. What has changed is the scale, breadth and complexity of what that oversight looks like in practice.

From manual assurance to holistic oversight

Historically, principal oversight across their AR network relied heavily on manual review, file sampling and periodic assurance. In an era of slower communication and face-to-face interactions, this approach was serviceable.

Today’s landscape is different. The volume and velocity of data, the complexity of digital channels and ways of doing business, and the speed of transactions mean that manual processes alone cannot keep pace.

What is emerging, and what will be increasingly important as the regime evolves, is a governance approach that is structured, policy-driven and continuously visible. Rather than retrospective effort, oversight becomes a proactive, measurable part of day-to-day operations.

This requires a structured, holistic approach to oversight, with clear rules of engagement to be a trusted AR within the network, teamed with oversight technology that is flexible, scalable and able to supervise on mass, across complex AR networks.

However, it is important to note that technology shall never be replacing human judgement. Instead, technology should amplify the reach and consistency of supervision, allowing compliance and risk professionals to apply their skills where they add most value.

Platforms (like Fingerprint) supercharge this progression from reactive to proactive AR oversight, embedding industry best practice regulatory policy into automated risk detection, offering streamlined, repeatable monitoring workflows and supervisory frameworks so that principals can scale their networks with confidence, not friction.

For those early adopter principals getting ahead of the technology game, effective oversight is no longer a regulatory burden, but a source of operational clarity, strategic stability and an enabler to growth.

The next forty years

The Appointed Representative Regime has quietly underpinned four decades of financial entrepreneurship in the UK. It has supported advisers, insurers, fintech innovators, consumer lenders, launching funds, asset managers and international entrants.

The proposals now under consultation do not signal the end of the model. They illustrate its maturity, and the willingness of government and regulators to refine it in ways that protect consumers and markets, while preserving its economic benefits.

Forty years on, the regime is not showing its age.

It is entering into one of its most strategically important phases yet. One in which innovation and accountability can be balanced with confidence and clarity.

If the first forty years unlocked market access, the next forty will define how that access is scaled responsibly, strengthening both the competitiveness and the credibility of the British financial sector.

And that is a future worth celebrating.

Want to learn more about how we support principal and regulatory hosting networks?

Get in touch! We’d love to have a chat about how to future proof your network’s next 40 years of operations with fit for purpose oversight technology.